Amortization vs. Simple Interest Loans: The Ultimate Guide

Amortization vs. Simple Interest

The main difference between amortizing loans vs. simple interest loans is that the amount you pay toward interest decreases with each payment with an amortizing loan. With a simple interest loan, the amount of interest you pay per payment remains consistent throughout the length of the loan. Amortizing loans are more common with long-term loans, whereas short-term loans typically come with a simple interest rate.

If you’re in the market for a small business loan, you’re likely to encounter terms you might not be familiar with. One of the most common areas of confusion for novice business owners is amortization vs. simple interest loans.

The difference between amortization vs. simple interest lies in how you will pay back your loan. It’s important to understand what each one means so you can pick a loan that makes the most sense for your specific business situation.

In this guide, we’ll explain how amortizing and simple interest loans work, show you an example of both in action, and explain why you might want to go with one over the other. Let’s start with basic definitions of both amortizing and simple interest.

What Is Amortization?

When it comes to loans, amortization refers to a loan you’ll gradually pay off over time in accordance with a set schedule—known as an amortization schedule. An amortization schedule shows you exactly how the terms of your loan affect the pay-down process, so you can see what you’ll owe and when you’ll owe it.

With an amortization schedule, you can compare payment schedules when you’re shopping for loans, break down your payments into an exact payment plan, and compare that payment schedule to your regular cash flow.

Loans can amortize on a daily, weekly, or monthly basis, meaning you’ll either have to make payments every day, week, or month. With amortizing loans, interest typically compounds—and your payment frequency will determine how often your interest compounds. Loans that amortize daily will have interest that compounds daily, loans that have weekly payments will have interest that compounds weekly, and so on and so forth.

Most importantly, amortizing loans start out with high interest payments that will gradually decrease over time. This is because with each payment you’re only paying interest on the remaining loan balance. So your first payment will feature the highest interest payment because you’re paying interest on the largest loan amount. With subsequent payments, an increasing amount of the payment will go toward the principal, since you’re paying interest on a smaller loan amount. Keep in mind, though, while the amounts you’re paying toward interest and principal will differ each time, the total of each payment will be the same throughout the life of the loan.

Amortization Example

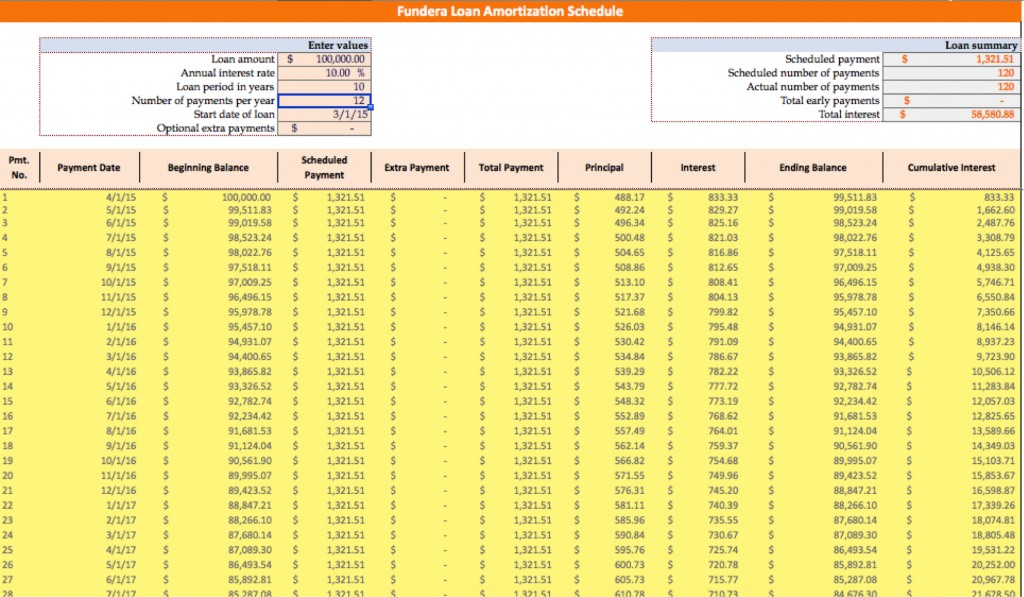

Now that we understand the basics of amortization, let’s see an amortizing loan in action. Let’s say you’re offered a three-year amortizing loan worth $100,000 with a 10% interest rate and monthly payments.

Once you do the math, you’ll find that each monthly payment amounts to $3,226.72. If you multiply this number by 36 (the number of payments you will make on the loan), you’ll get $116,161.92. This means you’re going to pay $16,161.92 in interest (assuming you don’t pay off the loan early).

Because the loan is amortizing, your first handful of loan payments will pay off more of the interest than the principal. To find out how much you’ll pay in interest, multiply the $100,000 balance owed to the bank by the 10% interest rate. You then divide the number of payments per year, 12, and get $833.33. This means that in your first loan payment, $2,393.39 is going toward the principal and $833.33 is going toward interest.

For the second payment, you now owe the bank $97,606.61 in principal. You’ll still pay $3,226,72, but this time you’ll only pay $813.38 in interest, and $2,413.34 in principal. This is because $97,606.61 x 10% divided by 12 is $813.38.

By the time you reach the final payment, you’ll only have to pay interest on $3,226.72, which is $26.88.

What Is Simple Interest?

At this point, we’ve already talked quite a bit about interest. But as a refresher, interest rate is the percentage a lender charges a borrower (you) to borrow a sum of money. This interest rate is quoted as a percentage of the amount of money you borrow. As the borrower, the amount you pay in interest is the cost of debt. For the lender, the interest rate is considered the rate of return.

Based on the interest rate you’re quoted, you will pay back a portion of your loan plus interest and other fees in accordance with your repayment schedule (amortizing or otherwise).

Simple interest is a specific type of interest you may be quoted on your loan. The first thing to understand about simple interest is that it’s a fixed interest rate, meaning the interest rate you are quoted when you take out your loan remains the same throughout the life of the loan (as opposed to adjustable rates, which fluctuate with the Market Prime Rate).

Simple interest is called simple interest because it is the simplest expression of your interest rate. Simple interest is the interest you’ll pay a lender in addition to the principal and is expressed as a percentage of the principal amount.

Here’s the simple interest rate formula:

Simple Interest = Principal x Interest Rate x Duration of Loan (years)

In our previous example of an amortizing loan, the simple interest rate was 10%, and the simple interest on the loan was $16,161.92.

Factor Rate

Factor rate is a simple interest rate expressed as a decimal instead of a percentage. If your simple interest rate is 12%, then your factor rate is 1.12. So if you take out a $100,000 loan with a 1.12 factor rate, you’ll repay $12,000 in interest because $100,000 multiplied by 1.2 = $12,000.

Simple Interest Example

Let’s see an example of a loan with a simple interest rate to understand how it differs from an amortizing loan.

Say you’re offered a six-month short-term loan of $100,000 with a factor rate of 1.2. You can tell right away that the total loan amount you’ll be required to pay back is $120,000 when you factor in interest.

This shorter-term loan has daily payments—22 days out of every month. This amounts to a total of 132 payments over the six-month term. Divide $120,000 by 132 and you’re left with $909.09. This is the amount that you’ll pay every day. To find out how much goes to principal and how much goes to interest, divide the principal and the interest by the number of payments you’re required to make.

When you do this, you’ll find that $757.57 of every loan payment goes toward the principal ($100,000 / 132) and $151.51 of every payment goes toward interest ($20,000 / 132). Unlike amortizing loans, each simple interest loan payment will have the same amount go toward interest and the principal.

Amortization vs. Simple Interest: Key Differences

These examples help us see some key differences between simple interest vs. amortization. For starters, with an amortizing loan, with each subsequent payment, you’ll pay more toward principal and less toward interest. With a simple interest loan, you’ll pay the same amount toward both principal and interest with each payment.

Amortizing loans also tend to have compounding interest, whereas simple interest loans have (you guessed it) simple interest. If your loan has a simple interest rate, the interest is calculated only on the principal amount.

A compounding interest rate means the interest is calculated both on the principal loan amount and on the accumulated interest. The rate at which compounding interest accrues depends on the compounding frequency—daily, weekly, or monthly—which typically matches the payment frequency, so the more payments you make, the more compound interest you’ll accrue.

The last key difference is that amortizing loans tend to be longer-term loans, whereas simple interest loans are often short-term financing solutions. Because of this, amortizing loans tend to have a higher cost of capital—you’re payments may be lower, but you make more of them so it winds up costing you more in the long run.

Simple interest loans have a lower cost of capital—meaning you’ll pay less overall—but each individual payment will be higher and could strain your cash flow.

Also keep in mind that your cost of capital could shift dramatically if you decide to pay off your loan early. Some amortizing loans will allow early repayment, thereby erasing any additional interest you’d otherwise have to pay. With a simple interest loan, you’re more likely to incur a prepayment penalty, as you’re paying the same amount to interest on every scheduled payment and the lender is counting on that money.

Make sure you talk to your lender about your loan terms before signing any loan agreement. We also recommend asking your lender to provide you with an APR, or annual percentage rate. The difference between APR and interest rates is that APR provides a more comprehensive look at how much you’ll pay when you take out a loan.

It factors in interest rate along with any fees you pay for borrowing (origination fee, application fee, closing fee, etc.). APRs also take into account the repayment term of your loan. Basically, it’s the total price of borrowing money expressed in terms of an interest rate.

Simple Interest vs. Amortized Loan: Which Is Right for You?

With the knowledge of amortization vs. simple interest, you should now be better equipped to pick out a loan that helps your business meet its financing needs. If you’re looking for a quick capital injection, a simple interest loan is probably right for you. If you need a large amount of financing and longer repayment terms, an amortizing loan will be less disruptive to your cash flow.

Ben Johnson

Ben Johnson is a content marketer at Proof, a Y Combinator-backed startup that provides real-time social proof software. Over 15,000 sites trust Proof to help increase their conversion rates.

Featured

QuickBooks Online

Smarter features made for your business. Buy today and save 50% off for the first 3 months.