State of Small Business Lending: Spotlight on Women Entrepreneurs

Fundera’s quarterly report, The State of Online Small Business Lending, lets us put all the data we have covering small business loan eligibility and borrowing trends to good use. The more educated and aware entrepreneurs are, the better decisions they can make when it comes to financing their businesses—we really believe that.

This quarter, we decided to take a closer look at an incredibly important topic: women in the world of small business. When compared to their male counterparts, how eligible are female entrepreneurs for business financing? What sorts of loans do they get, for how much money, and at what rates? Are there substantive differences in categories like credit score, annual revenue, and industry? In short, do women entrepreneurs have a harder time financing their businesses through business loans for women specifically?

Unsurprisingly, the results of our deep dive weren’t too encouraging—but we’re confident that alternative lending can be a platform for greater equality in the business financing industry. Transparency is just the first of many steps, but it’s a vital one.

You can access a PDF version of the report here and contact us with any questions, comments, or concerns at transparency@fundera.com. We look forward to changing the industry with you.

Main Takeaways:

- Female entrepreneurs ask for roughly $35,000 less in business financing than men.

- Only 1 in 4 applicants for business financing through Fundera were women, and a similar percentage of women end up receiving financing relative to men.

- However, women ask for $35,000 less on average than men do, which is consistent with trends underscored in the broader economic literature highlighted below that women employees tend to ask for smaller raises, and at a lower frequency, than their male counterparts.

- Women get approved for debt funding at a lower rate than men, but even more startlingly, women are likely to pay higher rates and receive less debt funding than male counterparts.

- While women are less likely to receive business credit than men, the difference is marginal: roughly 32% of women business owners are approved for credit, versus 35% for male entrepreneurs.

- That difference notwithstanding, of the women who do secure debt financing, they are more likely to receive a shorter-term loan with less capital and significantly higher interest rates.

- This dovetails with the tendency in venture capital to invest significantly more in male-owned than female-owned businesses: women have received only 7% of venture capital raised in the U.S., and only 10% of venture capital worldwide between 2010 and 2015.

- Women entrepreneurs get offered smaller loans across every product, from the same groups of online lenders, with no exception, and pay significantly higher interest rates than men do

- While SBA talking points and a study often cited by the agency from the Urban Institute claim that SBA loans are three to five times more likely to go to women or minority-owned businesses than conventional business loans are, our data paints a difference picture of equality for SBA financing.[1] Even among SBA loans, women receive 2.5 times less money than men do: on average, women get $59,857 while men receive $156,279.

- Whatever the cause, this demonstrates a sizable disadvantage women face in growing their businesses with debt financing. SBA loans, in particular, are meant to encourage even new and small businesses. This data falls in line with the Urban Institute’s research revealing that women-owned businesses only account for 4.4% of all dollars lent to small businesses each year and Forbes’ research highlighting that they generally receive just 80% of the capital when compared to men.[2][3]

- Lower financing amounts likely lead to slower growth for women-owned businesses and, ultimately, a smaller impact on the national economy.

- On average, women pay 6.4 percentage points and 5.4 percentage points higher rates for personal loans and short-term loans, respectively, than male entrepreneurs do.

- Women entrepreneurs have lower credit scores than men, with a 15-point difference between their averages.

- Credit score is the single greatest driver of a loan’s APR, as well as a major factor in financing eligibility, so it is sad but unsurprising that women-owned businesses qualify for smaller, more expensive business loans.

- The cause of lower credit scores among women entrepreneurs cannot be determined by our data alone, but it is likely related in some ways to the gender wage gap, which itself probably contributes to disproportionate debt-to-income ratios and credit utilizations between genders.

- On average, women-owned businesses make 30% less annual revenue.

- Annual revenue is another major factor in credit eligibility, although ironically, access to credit is also a factor that can determine a business’s annual revenue: by measuring its ability to grow.

- Women-owned businesses, with poorer access to credit, may be stuck in a cycle of more difficult growth.

- Roughly 60% of female entrepreneurs who applied for a loan through Fundera reported less than $250,000 in annual revenue.

Small Business Lending & Women Entrepreneurs

Women own nearly 1 in 3 small businesses in the United States, which means female entrepreneurs run more than 10.6 million companies, account for over $1.3 trillion of revenue, and employ nearly 8 million workers.[4]

Over the past 50 years, women entrepreneurs have made enormous strides towards equality. Although women-owned businesses accounted for 29% of all firms as of a 2007 study, they made up only 4.6% of companies in 1972.[5] Furthermore, women-owned businesses are getting started faster each year: the growth rate itself rose by 20% from 2002 to 2007, according to the Senate’s 2014 report on 21st century barriers to women entrepreneurship. This trajectory outpaces all other types of firms: women-owned businesses added roughly half a million jobs between 1997 and 2007, even while all other categories of companies lost jobs. And since the recession, women entrepreneurs are second only to publicly-traded companies in terms of job growth, with 274,000 net new jobs since 2007.[5]

Women entrepreneurs are also more confident in growth than their male counterparts, according to a recent study by Bank of America.[6] 54% of women small business owners expect their revenues to increase over the next year, while only 48% of men feel the same. In the words of Sharon Miller, managing director and head of Small Business at Bank of America, “Female entrepreneurs are excited about the future and focused on the success of their small businesses. They are demonstrating much greater levels of optimism than their male counterparts.” And interestingly, although 77% of female business owners say the glass ceiling exists, only 46% report feeling limited by it in some way.

In addition to their value to the national economy, women entrepreneurs also tend to be uniquely successful because of their differentiations. According to one study by the Centre for Entrepreneurs, women entrepreneurs are more interested than their male counterparts in being serial business owners.[7] In addition, they describe themselves more often as financial risk-takers, while also being more cautious of “foolhardy” choices.

Unequal Access to Business Financing

Yet for all that, women-owned businesses still only make up 4% of the national revenue and 6% of the workforce, according to the Urban Institute: a disparity which some attribute, at least in part, to unequal access to business financing.[2]

It is commonly said that women only receive 80% of the capital men do when searching for funding.[3] They receive just 16% of all conventional small business loans made each year and are 5 percentage points less likely to receive a loan than male entrepreneurs are.[2][8]

Building on these studies, Fundera’s data shines a light on several notable differences between men and women entrepreneurs as both business owners and business borrowers.

Of the 8,423 business owners we asked to submit a gender identification, roughly one-quarter (2,212) self-identified as women and three-quarters (6,211) identified as men. Out of this group, 887 successfully received funding: 669 men and 218 women. In other words, only 25% of funded small business financing applicants were women, which is in keeping with the percentage of women who filled out Fundera’s common application in the first place.

While these two groups shared many similarities across a number of categories, there were several metrics that demonstrated a significant difference between genders. Notably, our data tells us that, on average, women entrepreneurs are less creditworthy than male entrepreneurs, make less annual revenue, and own younger businesses. Moreover, we also found that women ask for less financing and receive fewer loans, for lower amounts, with higher interest rates.

Women Entrepreneurs & Business Financing

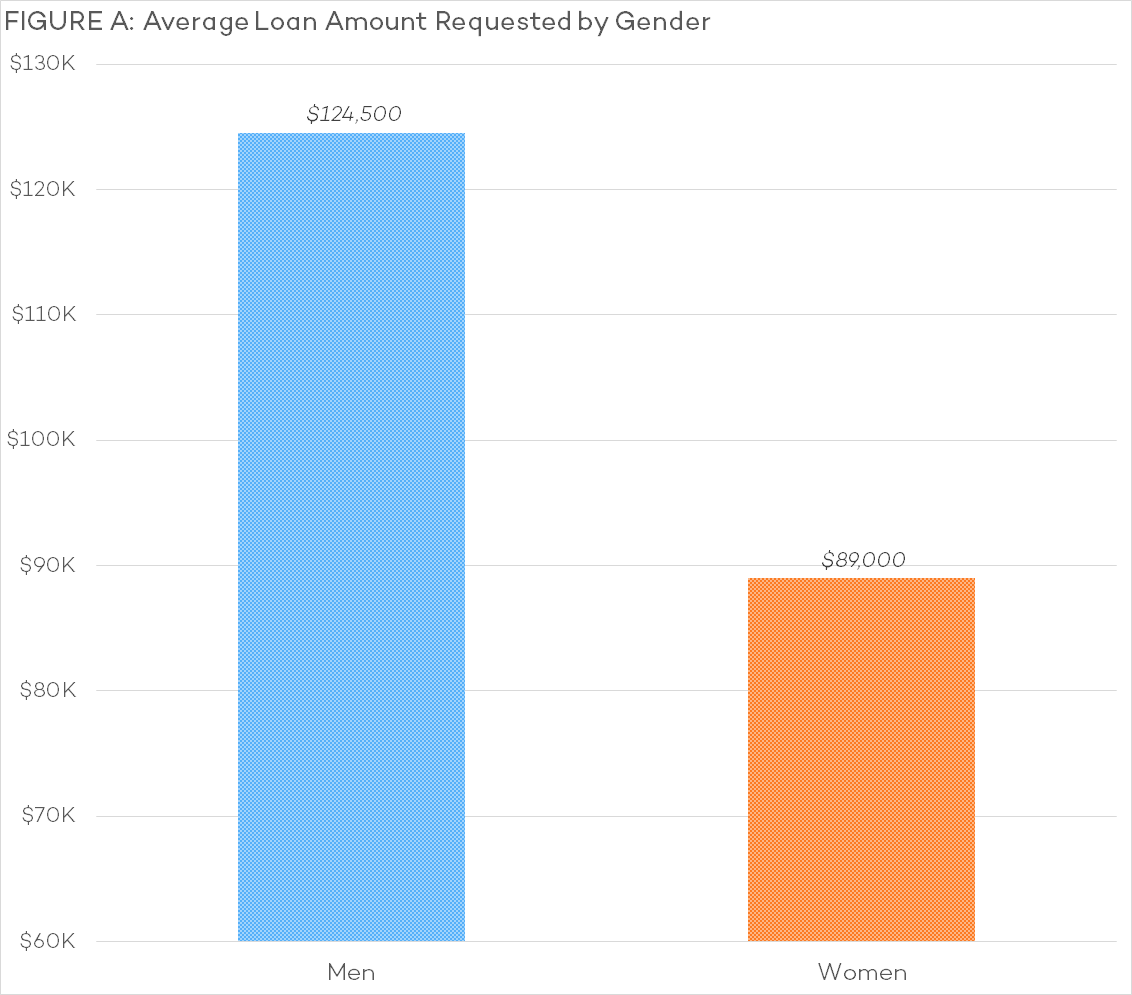

A. Women Ask for Less Money

Figure A shows the average loan amount requested by small business financing applicants, broken down according to gender. According to Fundera’s data, women ask for $89,000 in debt financing on average, while men ask for $124,500 on average—reflecting a difference of about $35,000. While this may have a number of causes, including the trends of lower eligibility we will point out later, it could also contribute to a discrepancy between actual loan amount funded.

There’s little doubt that this gap is due in part to the fact that women-owned businesses make less revenue and tend to have lower credit scores than male-owned businesses do, according to Fundera’s data, which we highlight further below. Interestingly, this trend is also shown in the broader economic literature. As a case in point, research by economist Linda Babcock at Carnegie Mellon University reveals that 4 times as many men as women ask for a raise and only 25% as many women as men negotiate their starting salaries—both of which contribute to the gender pay gap.[9][10] These data points all indicate a larger trend in women either undervaluing themselves, feeling limited by the social backlash against asking for a salary increase according to a study by Babcock alongside Hannah Riley Bowles of Harvard University, or both.[11]

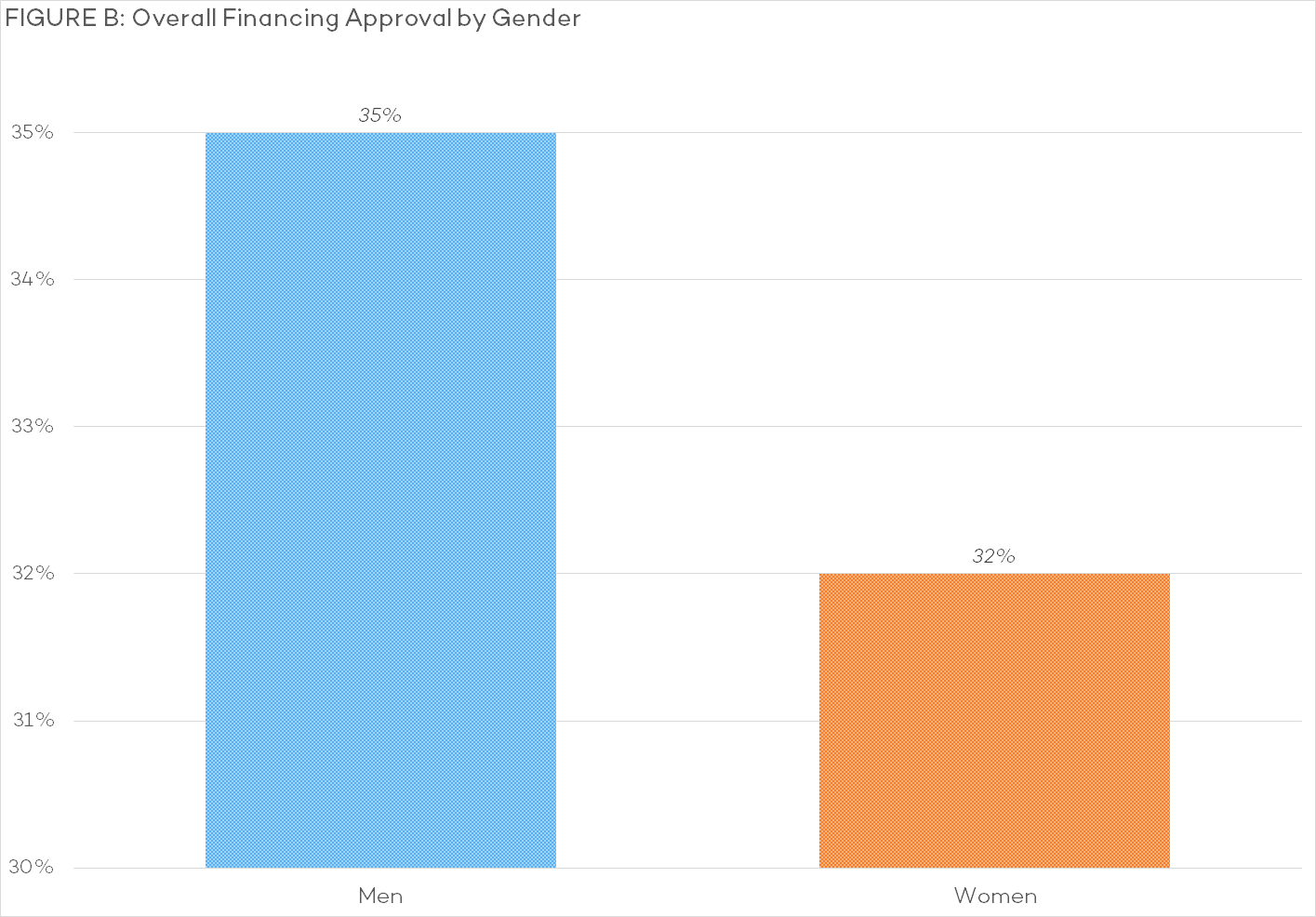

B. Women Get Turned Down More

Figure B highlights approval rates, including pre-qualified offers and final offers, for every type of business on Fundera’s marketplace across our 30+ small business credit providers, and across all product types they offer on our platform. On average, women-owned small businesses are approved for financing at a rate of only 32%, a full three-percentage points lower than approval rates for male-owned small businesses.

While it is lamentable that approval rates for women-owned businesses are lower than for male counterparts, even if only slightly, the more alarming statistic concerns the type of financing for which women business owners are more likely to be approved. In fact, women who are successful in getting approved for debt financing end up receiving more shorter-term funding, which represents the smallest loan sizes and most expensive interest rates on offer to any small business borrower.

Figure G (below) highlights percentage breakdown of each credit product on Fundera’s platform by gender, underscoring that women-owned small businesses are more likely to receive short-term funding: roughly 30% versus nearly 23% for men. While this type of funding has among the fastest time to from approval to funding rates in the small business credit market, it is also among the most expensive, with average percentage rates (APRs) varying from 14% to 50% or higher.

Also noteworthy is the gap between the concentration of men and women entrepreneurs for the federally-backed Small Business Administration loans, which generally offer the most affordable business financing and largest average loan sizes available. For example, APRs and average loan sizes for SBA debt financing vary from 6% to 10% and up to $5 million, respectively. Women are about half as likely as men are to receive an SBA loan, with only 3.2% of all women receiving an SBA loan, versus 6.4% for male business owners. SBA eligibility relies more on credit score than annual revenue and time in business, often requiring a credit score of 700 or above.

This data may directly counter research from the Urban Institute, as well as talking points disseminated by the SBA, which has highlighted that SBA loans are more likely to go to women and minority-owned businesses than conventional loans do.[1]

This issue is not specific to debt financing, however. According to TechCrunch’s study on women in venture capital, only 10% of venture capital dollars worldwide, between 2010 and 2015, went to businesses with at least one female owner.[12] Meanwhile, women-owned businesses have received just 7% of all venture capital within the United States.[13] Similarly, only 15% of seed capital went to the same category of startups.

In addition, women entrepreneurs are not taken as seriously by investors. One study from Harvard Business School, Wharton School, and Massachusetts Institute of Technology’s Sloan School of Management determined that the gender of an entrepreneur would affect the success of their business pitch in a competition, even when their pitches were identical.[13]

According to this study, “the gender imbalance in entrepreneurship has been attributed to a persistent incongruence between personality attributes ascribed to women and personality attributes ascribed to entrepreneurs.” In other words, the idea of a “woman entrepreneur” is seen as contradictory by many, based on the personality traits that both women and entrepreneurs are stereotypically believed to have.

Though the rate of women engaging in entrepreneurship has risen over the past few years, the startup landscape remains male-dominated. Debt financing is a more equitable funding solution for both genders, but there is still a slight bias against women business owners.

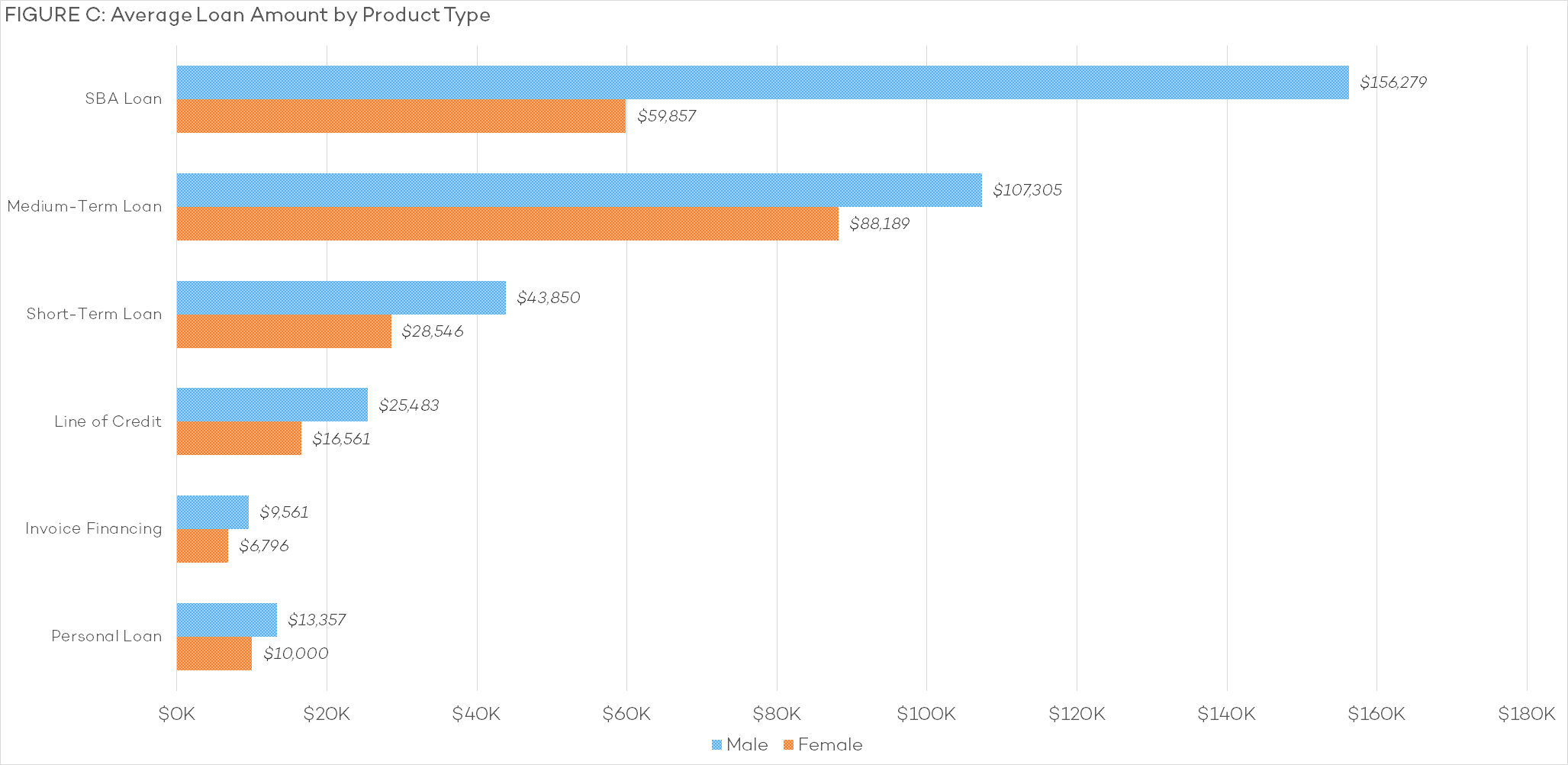

C. Women Receive Smaller Loans

Figure D highlights the average loan amount that Fundera’s customers receive, broken down by product type and gender. This graph makes it obvious how much less women entrepreneurs receive in financing across every kind of business loan, from lines of credit to invoice financing.

Not only does half the proportion of female business owners receive SBA loans when compared to male business owners, but they also receive 2.5 times less money from those same loans. According to the SBA, 21.3% of its loans (constituting 16.2% of the total dollar amount it funds) go to women entrepreneurs.[14]

In fact, it is clear that women entrepreneurs get offered smaller loans across every product, from the same groups of online lenders, with no exception. Whatever the cause, this demonstrates a sizable disadvantage women face in growing their businesses with debt financing. SBA loans, in particular, are meant to encourage even new and small businesses.

This data falls in line with the fact that women-owned businesses only account for 4.4% of all dollars lent to small businesses each year and that they generally receive just 80% of the capital when compared to men.[2][3]

D. Higher Interest Rates for Women

Finally, Figure D displays the average effective APR—a substitute for interest rates, plus other rates a borrower will have to pay—according to loan type and gender. According to Fundera’s data, women face higher interest rates nearly across the board. Their lower SBA loan APRs are almost certainly due to their SBA loan amounts being only nearly 40% of the SBA loans that male entrepreneurs secure.

However, the discrepancy in APR does not seem to reflect the difference in loan amount. While men receive over 50% more than women for short-term loans, women on average pay a 13% higher interest rate for that same product, for example.

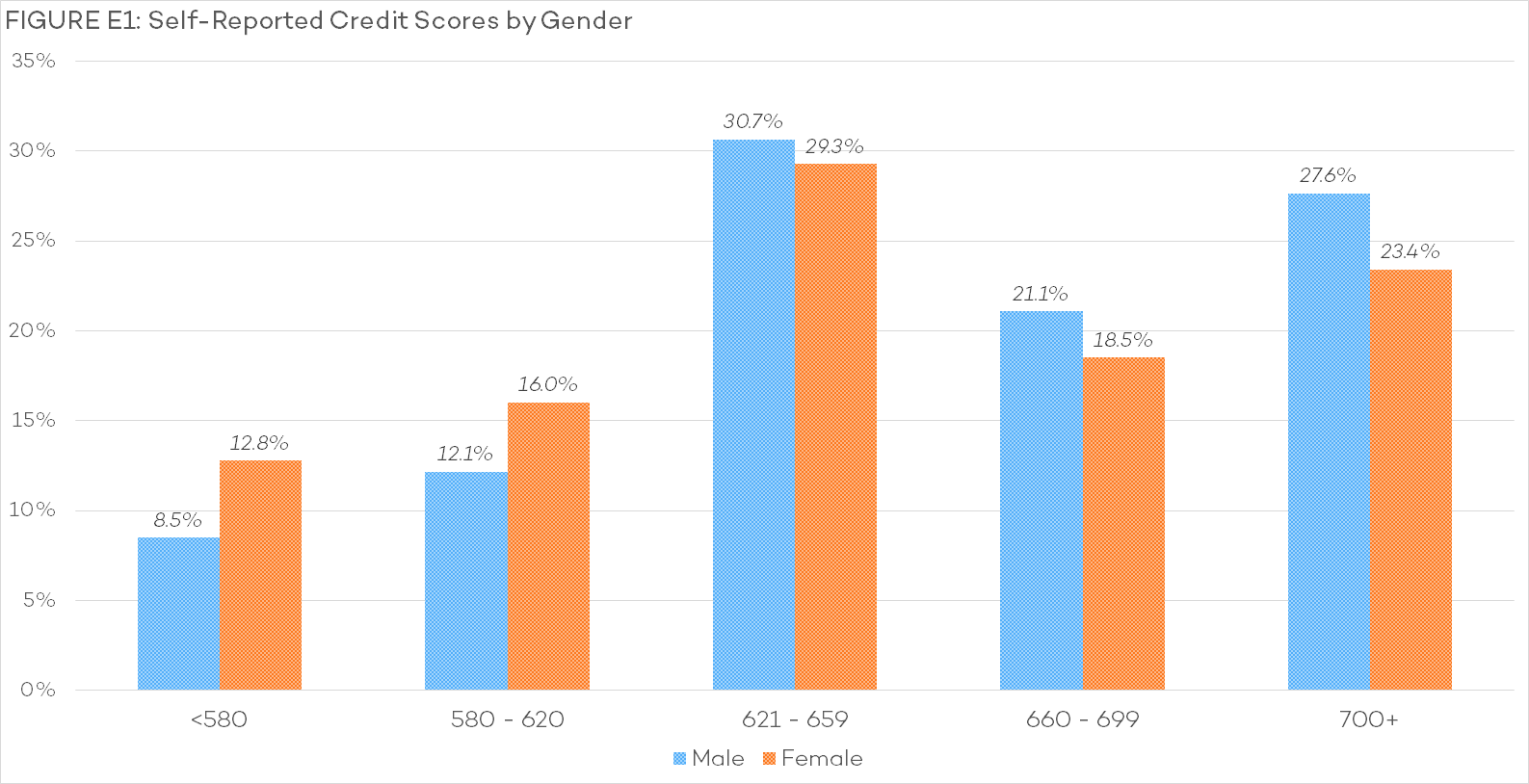

E. Women Entrepreneurs Have Lower Credit Scores

As indicated by Figure E1, which reports the self-reported credit scores of all small business owners who applied for financing through Fundera, women entrepreneurs report lower personal credit scores than men do.

The most significant differences are in categories of especially high impact regarding these business owners’ credit eligibility: below 550, from 550 to 650, and from 650 above are three general tiers of eligibility that business owners can be sorted into.

Credit score is one of the most important factors, if not the single most important factor, in determining a business owner’s financing eligibility. However, it cannot be determined by our data alone whether the trend of lower credit scores for women entrepreneurs is a cause of credit access imbalance, an effect resulting from other causes, or irrelevant. Given the importance of personal credit to qualifying for small business financing, though, its irrelevance is unlikely.

According to a recent report by Credit Sesame on credit and gender, the average credit scores for men and women are 630 and 621, respectively. And though men also own more debt than women do, they owe disproportionately: men tend to have lower debt-to-income ratios. They also maintain lower credit utilization, an important factor in one’s credit score, because their credit limits tend to be higher as a result of larger incomes, says Business Insider. Women are also slightly more likely than men to have one or more collections accounts, which can negatively impact their credit score.[15][16]

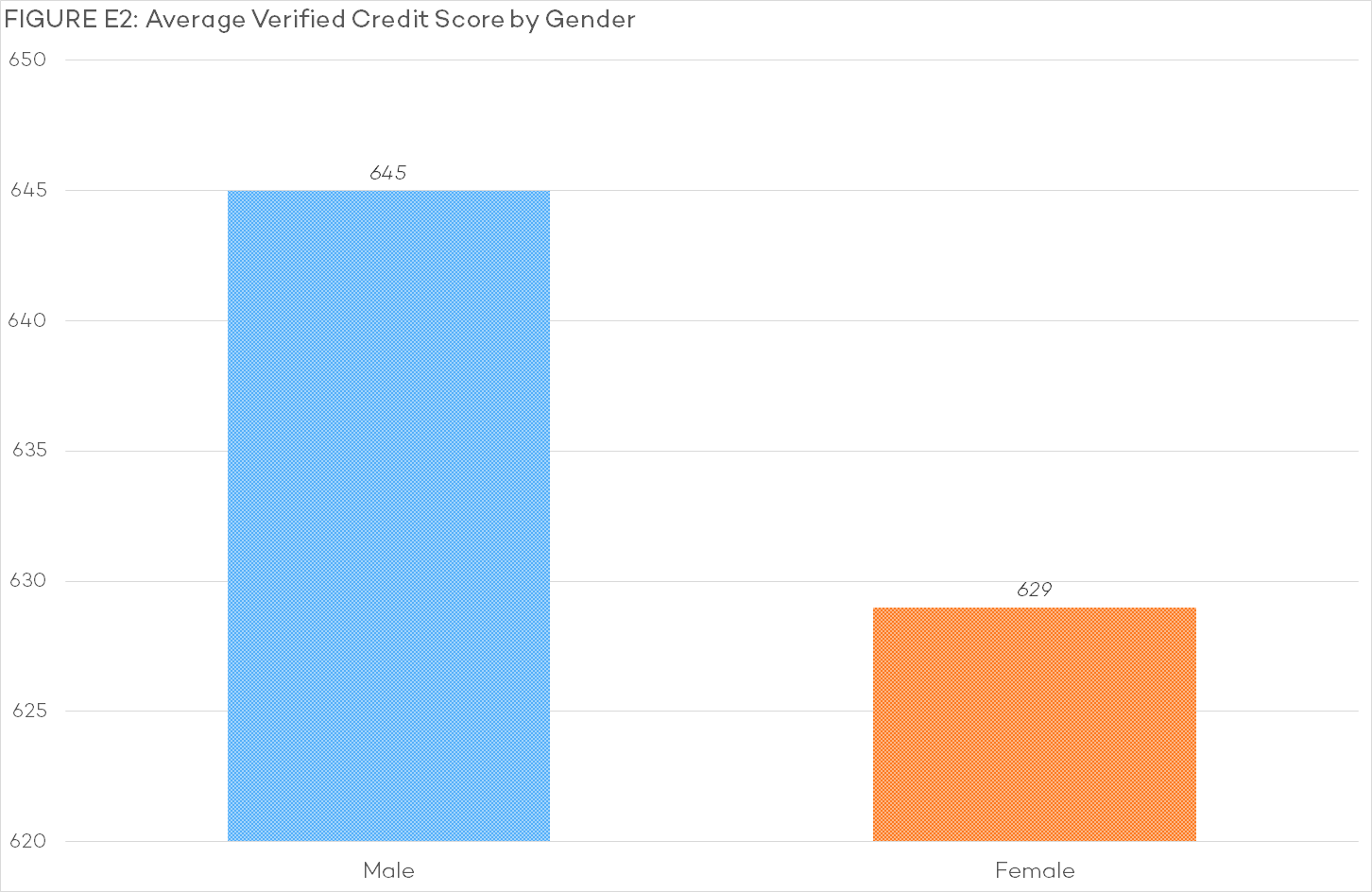

It appears that these trends of lower credit scores hold true for women entrepreneurs as well, both on average (as indicated by Figure E2) and across every credit score range. This very likely restricts women from accessing the kinds of loans that men are able to secure.

It appears that all business owners who submit a loan application through Fundera, and in so doing get their credit score verified, tend to have higher-than-average credit scores for their gender (630 for men and 621 for women). However, the discrepancy of average credit score between genders is even larger among business owners who applied for funding.

F. Less Annual Revenue for Women

Figure F1 breaks down the annual revenue buckets that Fundera’s business financing applicants fall into by gender. On average, female business owner applicants make 30% less revenue than male business owner applicants.

It is clear that a larger portion of women-owned businesses fall into lower revenue buckets, which may partially account for the fact that all women-owned businesses only make up 4% of the national revenue. In fact, roughly 60% of female entrepreneurs who applied for a loan through Fundera reported less than $250,000 in annual revenue, while less than half of male entrepreneurs reported the same.

Like credit score, annual revenue is an important factor in credit eligibility. Certain affordable types of loans, in particular, open up more at the $400K, $600K, and $900K milestones, each of which higher proportions of male-owned businesses have reached.

This follows the larger and long-standing trend of women making less money than men, both as entrepreneurs and employees. On average, full-time women earn around 78 cents for every dollar earned by a full-time male employee, according to The American Association of University Women.[17][18] While that statistic has improved from 59 cents in 1963, it still means women bring less money to their households, have smaller cash cushions, save less for retirement, get offered lower credit card spending limits, and so on.

Although we cannot prove cause and effect here, it is no far stretch to connect the gender wage gap with lower credit scores, which leads to less business financing—and stunted growth in the form of lower revenue. With smaller cash cushions, late payments are a larger hazard for women; with lower spending limits but disproportionately lower debts, their credit utilization is higher. These factors both negatively contribute to credit score.

Furthermore, although it is beyond the bounds of Fundera’s data, it is important to note that the gender wage gap varies according to race…

…And age:

Data for the above graphs was taken from The American Association of University Women, Spring 2016. Geography and education level, as well as other factors, also have an impact.[17][18]

G. Women Get Shorter-Term & More Expensive Products

Figure G shows what percentage of Fundera’s funded applicants, by gender, acquired which types of business loans. In terms of the loan products men and women secured through Fundera, men received more affordable financing while women took out smaller and more expensive loans.

Short-term and medium-term loans are an easy way to see this difference:

They are structured similarly, but short-term loans have higher rates and lower eligibility standards. Almost 30% of women settled for the more expensive short-term loans, while only around 20% men did so. Meanwhile, one-third of men secured affordable medium-term loans, but just a quarter of women qualified.

Also noteworthy is the disjunct between men and women for the federally-backed SBA loans, almost always the most affordable business financing available. 6.4% of male business owners secured an SBA loan, while only half—3.2%—of women got the same. SBA eligibility relies more on credit score than annual revenue and time in business, often requiring a credit score of 700 or above.

H. Women-Owned Small Businesses by Industry

Figure H demonstrates where men and women tend to differ in terms of the kinds of businesses they choose to manage. Fundera categorizes business owners into 65 different industry types, although most entrepreneurs fit into 25 or so, and only 10 are featured here.

Many seem to follow what we might consider to be the stereotypes of typically gendered industries, such as beauty salons, construction, fashion, and trucking. Women run beauty salons, barber shops, and spas nearly 5 times as much as men, while construction is almost 3 times as popular for men as it is for women.

These proportions roughly correlate with the Bureau of Labor Statistics’ census on employment by industry, sex, race, and ethnicity.

I. Women Have Younger Businesses

Figure I highlights the average age of the businesses that applied for financing according to the gender of their owners.

Another significant metric for credit eligibility, time in business across genders does not vary much, except by showing that a slightly greater proportion of women-owned businesses are 2 years old and younger.

This data is notable for its regularity: with such little differentiation between genders, it is unlikely that time in business impacts one gender’s eligibility in a significant way. Again, it may be possible that a shorter average time in business affects access to financing, or the other way around.

In addition, it is interesting that the number of women starting new businesses is on the rise: women-owned businesses grew nearly 27% from 2007 to 2012, while growth among all firms was only 2%. Fundera’s data appears to underscore that point, with a greater proportion of businesses younger than 1 year looking for financing belonging to women entrepreneurs than to men.

In Conclusion

Although our data only highlights a small portion of business owners searching for financing, one thing is clear:

There is a consistent and systemic disparity in how men and women entrepreneurs can finance their small businesses. Women receive fewer, smaller loans for higher interest rates, and this doubtless contributes to their disproportionately small influence over the national economy. According to a report by the United Nations’ International Conference on Population and Development, the United States’s small business gender gap costs at least $800 billion, in addition to the many other advantages brought by a larger and more equitable credit economy.[19][20] Women also ask for less financing, in line with asking for fewer raises and less venture capital.

The causes of these issues are difficult to place exactly, but due to the importance of one’s credit score and annual revenue with regards to both qualifying for a loan and the terms of that financing, it is likely that the discrepancies between men and women entrepreneurs in these areas contribute to imbalanced small business credit access. These, in turn, are likely influenced by the gender pay gap, cultural perceptions of gender and entrepreneurship, and more.

Women’s access to business financing is not a woman’s issue; it is everyone’s issue. Fundera believes that improved transparency is the first of many steps we can take as a company and an industry to fix it.

A Note On Our Data

As a marketplace offering many different lenders and kinds of loan products, Fundera can evaluate data that includes all types of business owners and enterprises across the country.

Our data from February 2014 to June 2016 (Q2 2016, inclusive) is comprised of:

- More than 3,500 loans funded

- Over $175M funded

- Nearly 2,800 small business owners funded

- Customers with credit scores below 550 and above 700

- Customers with annual revenues below $50K and above $2M

- Customers from all 50 states and across many industries

- Businesses of all ages, from startups to 35+ year-old institutions

Although we’ve helped nearly 60,000 small business owners understand their financing options, only around 13.5% of our customers were asked to self-report their gender identifications. As a result, this report only covers:

- Over 8,400 small business applicants: around 6,200 men and 2,200 women

- Almost 900 funded small business owners: roughly 700 men and 200 women

While this data only makes up a portion of our total customer base, it is significant enough to glean insights about the larger trends that Fundera sees—and perhaps to reflect the online small business lending industry as a whole.

Recognizing Problems with Transparent Data

It should be noted that none of these factors necessarily contribute to a disparity in small business credit access, and if any do, they are doubtless only one among many. It is Fundera’s goal to be as transparent as possible, especially regarding such a sensitive and important topic, but it is also important not to oversimplify a complicated issue.

It is our hope that increased transparency will help our community recognize the problems underlying small business financing access and strive to create a fairer, more honest, and more prosperous industry together.

Looking Ahead

If you have questions or feedback about The State of Online Small Business Lending, please email transparency@fundera.com.

Access the PDF version of this report here.

Article Sources:

- Urban.org. “Key Findings From the Evaluation of Small Business Administration’s Loan and Investment Programs“

- Urban.org. “Competitive and Special Competitive Opportunity Gap Analysis of a 7(a) and 504 Programs“

- Forbes.com. “Why Women-Owned Firms Are Being Held Back“

- SBNOnline.com. “Why Women-Owned Startups are Desperate for Female Mentors“

- SBC.Senate.gov. “21st Century Barriers to Women’s Entrepreneurship“

- BusinessWire.com. “Bank of America Survey Finds Women Small Business Owners More Optimistic Compared to Men on Revenue and Growth Outlook“

- CentreforEntrepreneurs.org. “Women Entrepreneurs Show Appetite For Growth“

- WorldBank.org. “Do Banks Discriminate Against Women Entrepreneurs?“

- NPR.org. “Ask For a Raise? Most Women Hesitate“

- Psycnet.APA.org. “Who Goes to the Bargaining Table? The Influence of Gender and Framing on the Initiation of Negotiation“

- ScienceDirect.com. “Social Incentives for Gender Differences in the Propensity of Initiate Negotiations: Sometimes it Does Hurt to Ask“

- TechCrunch.com. “The First Comprehensive Study on Women in Venture Capital and Their Impact on Female Founders“

- PNAS.org. “Investors Prefer Entrepreneurial Ventures Pitched by Attractive Men“

- SBA.gov. “Women-Owned Businesses“

- CreditSesame.com. “Credit Score Men vs. Women“

- BusinessInsider.com. “How Being a Women Can Ding Your Credit Score“

- CNN.com. “Equal Pay Day: When, Where and Why Women Earn Less Than Men“

- AAUW.org. “The Simple Truth About the Gender Pay Gap“

- UNFPA.org. “International Conference on Population and Development“

- NewStatesman.com. “Gender Inequality Is Costing the Global Economy Trillions of Dollars Each Year“

Jared Hecht

Jared is the co-founder and CEO of Fundera, an online marketplace connecting small business owners to the best loans for their business. He writes frequently on small business lending and management.